Turkey’s Grand National Assembly passed a broad fiscal reform package last week, the centerpiece of which grants new residents a 20-year exemption from Turkish income tax on all foreign-source earnings and capital gains.

President Recep Tayyip Erdoğan, who first announced the measure at an Istanbul investment forum in late April, has 15 days to sign the bill and publish it in the Official Gazette before it enters into force.

Who Qualifies and What the Exemption Covers

The regime exempts foreign-sourced income from Turkish income tax for 20 years for individuals who move their tax residence to Turkey, provided they had no domicile or tax liability in Turkey during the previous 3 calendar years. Foreign-sourced income covered by the exemption will not need to be declared in an annual Turkish income tax return.

The exemption applies to dividends, foreign passive income, capital gains, and other overseas earnings. Domestic Turkish income continues to be taxed under the standard progressive scale, which runs from 15% to 40%.

Inheritance and gift tax for qualifying individuals is reduced to a flat 1% rate, replacing a progressive scale that previously reached up to 30%.

Turkey announced the package amid regional economic disruption caused by the Iran war. Finance Minister Mehmet Simsek said the reforms were intended to position Istanbul as a leading financial gateway and that the tax reductions are long-term and “here to stay.”

The Istanbul Financial Center’s chief executive told Reuters that the conflict affecting Gulf states had prompted dozens of companies with regional operations to explore relocating business to Istanbul.

The Broader Reform Package

The individual tax exemption is one component of a wider legislative package targeting both corporate and personal tax. The legislation broadens tax perks linked to the Istanbul Financial Center, with profits from overseas trade in which goods do not physically enter Turkey qualifying for a 95% corporate tax deduction, rising to 100% for firms operating within the IFC.

The package extends IFC incentives until 2047 and expands license fee exemptions from five to 20 years. Qualified personnel receive wage income tax exemptions worth up to three times the gross minimum wage, increasing to five times for IFC-based staff with participation certificates. The corporate tax rate for certified manufacturing and agricultural production companies will fall to 12.5% starting in 2027.

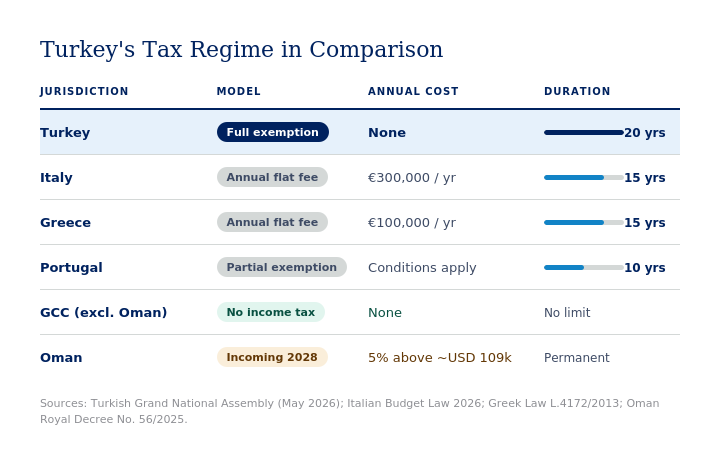

How It Compares With European and Gulf Tax Regimes

Turkey’s 20-year window is longer than any comparable program currently operating in Europe.

Italy’s flat tax regime, in force since 2017, allows new residents to replace ordinary Italian taxation on foreign-sourced income with a single annual substitute tax of €300,000, valid for up to 15 years. Domestic Italian income remains taxable at standard rates.

Greece’s non-dom regime charges a flat annual tax of €100,000 on worldwide income, regardless of the amount earned, requires a minimum investment of €500,000 in real estate, local businesses, or financial products, and runs for a maximum of 15 years, with no possibility of extension. Family members can be added for €20,000 per year each.

Portugal replaced its widely used Non-Habitual Residency scheme with the IFICI framework, which carries stricter eligibility conditions and a 10-year benefit period.

Turkey’s structure differs from European flat-tax models in that it provides full exemption from foreign income rather than a fixed annual substitute tax.

Within the Gulf, most GCC states have historically levied no personal income tax at all; a structural advantage that has made them perennial destinations for internationally mobile professionals and capital.

The UAE, the region’s most prominent financial hub, charges no personal income tax on either domestic or foreign-source income.

However, that landscape may be shifting; Oman has become the first GCC country to introduce a personal income tax, set to take effect on January 1, 2028. The law introduces a 5% income tax on natural persons whose annual gross income exceeds OMR 42,000, approximately USD 109,200.

The change is modest in scope, but it marks the first breach of the Gulf’s long-standing consensus on personal income tax.

Accessing the Regime: Turkey’s Citizenship by Investment Program

For most foreign nationals looking to establish Turkish tax residency and benefit from the exemption, Turkey’s Citizenship by Investment program is the most direct route to legal residency.

The program allows foreign investors to obtain Turkish citizenship in as little as 6 to 12 months by making a qualifying investment of at least $400,000 in real estate or $500,000 in other approved assets, including government bonds, bank deposits, or fixed capital investments.

Real estate purchased under the program must be acquired from a Turkish citizen or Turkish entity, paid through a Turkish bank, and is subject to a three-year holding period before it can be resold.

The program requires no minimum residency period or language test and allows applicants to include eligible family members, including spouses, children, and disabled dependents.

The citizenship route is particularly relevant to the new tax regime because establishing Turkish tax residency, the prerequisite for the 20-year exemption, requires a legal basis to reside in the country.